The Fair Pricing Playbook

A practical framework for Responsible AI in algorithmic pricing (2026)

Why fair pricing matters

Algorithmic pricing is now widely used in insurance and financial services, and advances in AI and machine learning have become central to how insurers assess risk, detect patterns in large datasets, and set prices. The fairness concerns this creates are not new, but they take a different form under automated, large-scale systems. Even when protected attributes such as race, gender, and religion are removed from a model, pricing systems can still produce discriminatory outcomes through proxy variables and opaque algorithms that are difficult to trace or challenge. The rapid adoption of AI and big data has created a regulatory grey area: direct discrimination is prohibited, but indirect discrimination through proxies and complex algorithms is not clearly specified or assessed in most markets (Frees and Huang 2023; Xin and Huang 2024).

Regulatory attention to these issues has grown substantially. Colorado and New York have each proposed rules requiring insurers to test pricing algorithms for unfair discrimination, and the European Union has enacted broader AI governance frameworks that apply to insurance. The EU AI Act classifies credit scoring and insurance risk assessment as high-risk AI applications, placing fairness obligations alongside broader requirements for transparency, human oversight, and accountability. Firms that cannot demonstrate fairness face legal exposure, reputational risk, and the practical challenge of defending pricing decisions under regulatory examination.

This playbook translates research from economics, statistics, actuarial science, and machine learning into a concrete four-step workflow that covers the full journey from defining what fairness means, to building fair models, to measuring who actually gains and loses, to auditing a deployed system. While the case studies use insurance data and draw on insurance regulation, the four-step framework applies to any sector where algorithmic pricing raises fairness concerns, including credit, housing, energy, and mobility. Three insurance case studies provide the technical depth needed for implementation.

Watch: Introduction to anti-discrimination insurance pricing

The four steps

Step 1 · Define fairness

This step surveys the different lenses of fairness and the criteria they imply. They cannot all be satisfied simultaneously, and the choice is a legal and policy decision, not a technical default.

Step 2 · Design fair pricing

Once a criterion is chosen, this step maps it to a concrete model design and shows where in the pipeline (inputs, training, or outputs) to enforce fairness, based on what regulation requires.

Step 3 · Assess impact

A fair cost model does not guarantee a fair market outcome. This step traces price effects through demand and competition, quantifying consumer welfare and firm profit by group after prices are set.

Step 4 · Audit the system

An audit tests whether a deployed system actually meets the standard. All protocol choices (criterion, tolerances, sample design) are fixed before examining any data. Results are pass, fail, or insufficient information.

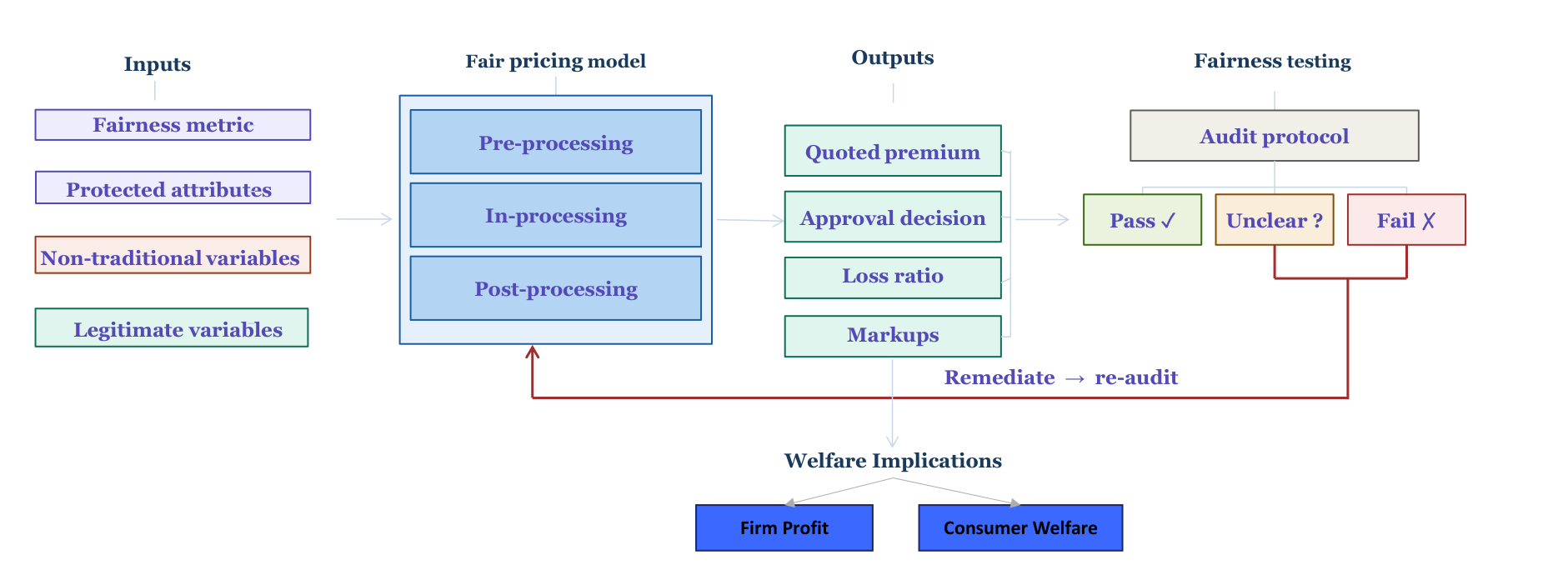

The pathway at a glance

The diagram shows how the four steps connect across model design, welfare assessment, and fairness testing. Steps 1 through 3 work together to inform a single decision, which fairness criterion fits a specific application or line of business. Step 2 shows the accuracy-fairness trade-off, how much predictive power a fairness constraint costs at the model level. Step 3 shows the welfare-fairness trade-off, how a fair cost model can still produce unequal market outcomes once price optimisation and demand enter the picture. Neither trade-off has a universal answer, which is exactly why these steps matter. Seeing both is what lets stakeholders choose a criterion in Step 1 that fits their product, market, and regulatory context, rather than defaulting to whichever criterion is easiest to implement.

What the research shows

| Step | Key references |

|---|---|

| 1 · Define fairness | Frees and Huang (2023); Xin and Huang (2024); Krafcheck et al. (2026) |

| 2 · Design fair pricing | Xin and Huang (2024) |

| 3 · Assess impact | Huang et al. (2026); Huang and Shimao (2026) |

| 4 · Audit the system | Huang and Hooker (2026); Xin et al. (2026); Xin et al. (2025) |

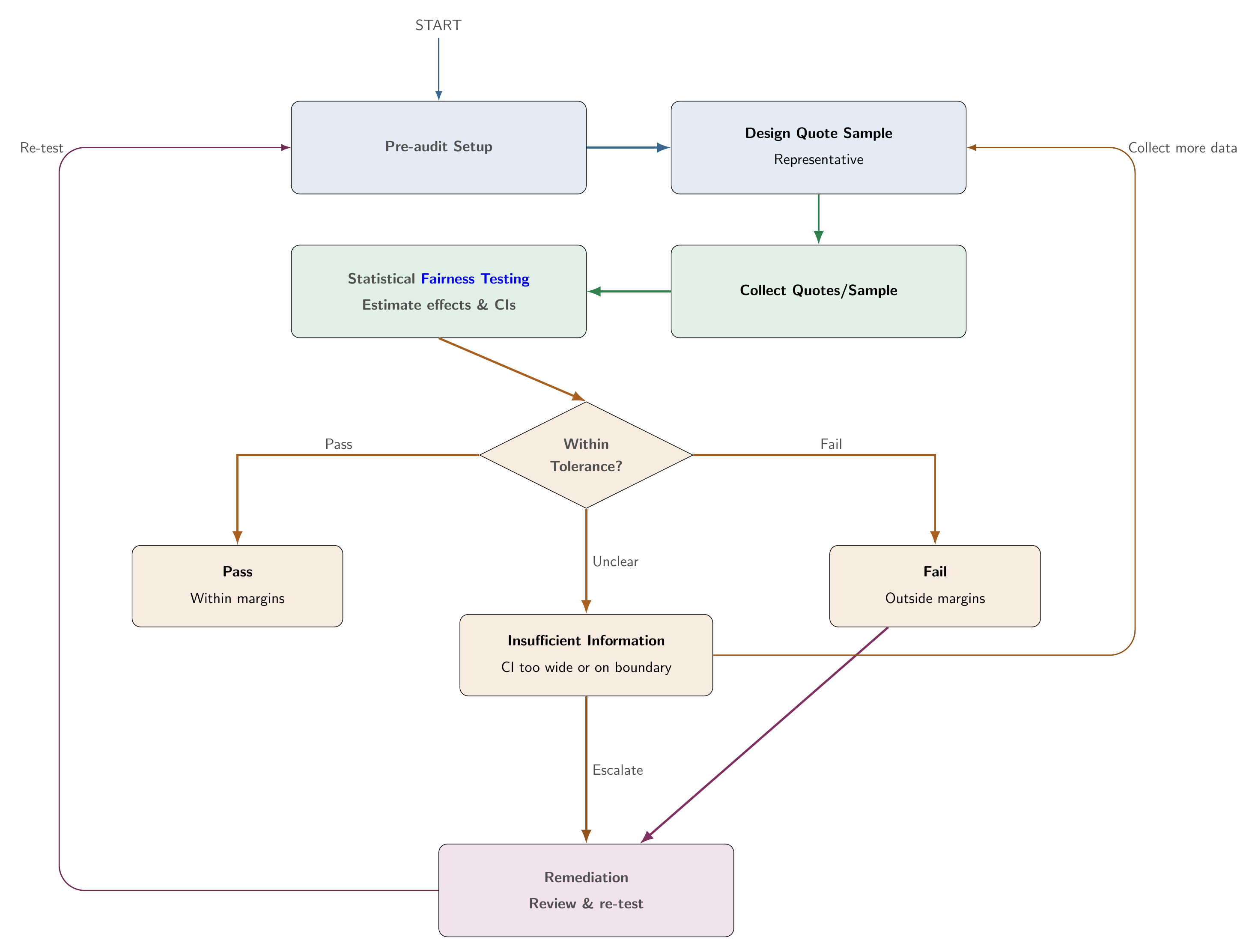

End-to-end audit flow

Step 4 follows an integrated Plan, Audit, Decide, and Improve protocol (Huang and Hooker 2026). All design choices are fixed before examining data.

| Phase | Actions |

|---|---|

| Plan | Select criterion (PD or CDP), legitimate factors, tolerance bands, representative sample |

| Audit | Collect prices and run statistical fairness tests with corrected inference |

| Decide | Pass, insufficient information, or fail (equivalence testing) |

| Improve | Remediate and re-test. Collect more data if result is unclear |

Full detail is in Step 4: Audit the system.

See the About page for author bio, acknowledgements, citation, and licence.